Written by: Bhawramaett Broehm, Senior Project Lead

After two decades of relatively flat load growth, electricity demand is rising again, driven in part by data centers, manufacturing expansion, and electrification. At the same time, the market for major generation equipment has tightened, supply chains remain constrained, and resource adequacy frameworks are placing greater emphasis on the ability to deliver dependable capacity during critical grid conditions. The result is a more complex planning environment, where supply and demand dynamics are increasingly uncertain, and utilities are being forced to reshape their approach to power supply planning.

Supply Chain & Capital Costs

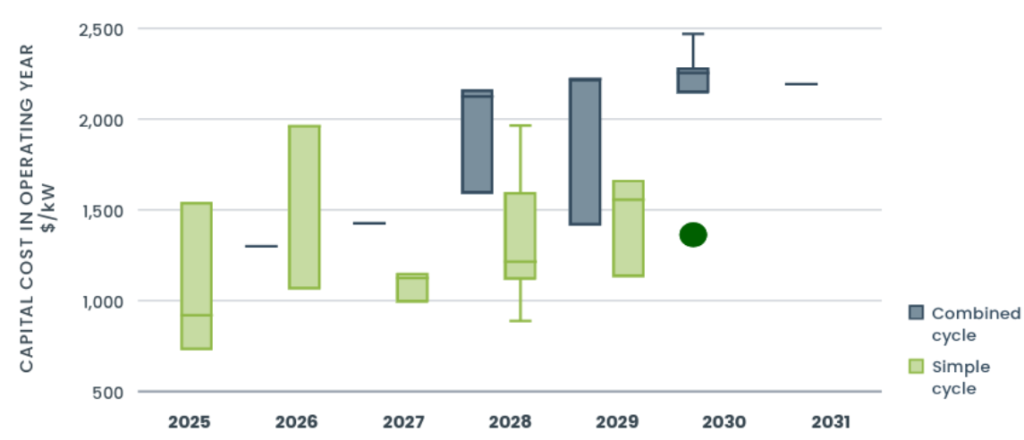

To emphasize the supply/demand dynamic uncertainty, one sobering near-term signal comes from the original equipment manufacturers (OEMs) of thermal generation resources. According to S&P, OEMs have been quoting lead times of five to seven years for gas turbines and project costs have increased by roughly 250% compared to a few years ago.1 In April, GE Vernova reported that gas power equipment backlog and slot reservation agreements increased to 100 GW, with an expectation of at least 110 GW by year-end 2026.2 Siemens Energy similarly reported record orders in its Q2 earnings call, with total order backlog reaching €154 billion.3 The elevated financial performance of major power generation OEMs demonstrates that demand for key generation and grid equipment is at record highs, order books are full, and suppliers have materially greater pricing power than in previous years. As a result, commonly used public capital cost datasets may understate current market realities, including the fact that labor shortages are contributing to higher costs and longer development timelines for thermal projects. 4 The following figure demonstrates the upward trend in gas turbine project costs.

Publicly available gas turbine project costs (Source: GridLab, Energy Futures Group, and Halcyon)

Together, rapidly increasing capital costs and extended lead times for traditional gas turbine resources will require resource planners to adapt to help electric utilities maintain reliability and affordability. A capacity need that may have conventionally been met by a large gas turbine project, may now require other technologies such as smaller, modular turbines, reciprocating engines, linear generators, and/or a mix of variable renewable energy and storage resources. Conversely, as OEMs prioritize larger deals for limited factory slots, smaller utilities may need to explore different contracting strategies, such as joint ownership with neighboring utilities, to strengthen their position in supplier negotiations.

Resource Adequacy

At the same time, generation economics go beyond traditional evaluation of capital and operating costs. Resource adequacy rules increasingly focus on how effectively resources contribute during the hours that matter the most for maintaining grid reliability, often referred to as “critical peak periods”. That shift is especially important as grids adopt effective load carrying capability (ELCC) frameworks. ELCC is an increasingly common resource accreditation methodology that assesses how much a resource contributes to system reliability during those critical peak periods.

While accreditation values for solar, wind, and energy storage vary across seasons and markets, consistent trends persist. In many ELCC-based frameworks, solar and wind receive fractional accreditation values that decline as penetration of these resources rises. Similar trends emerge for energy storage, albeit, typically at a slower pace, because it can more readily shift energy output into periods of highest risk, especially as the energy storage’s duration increases. The implication for resource planners is that a megawatt of nameplate capacity is not the same as a megawatt of dependable capacity. This distinction is increasingly important when evaluating resource economics and their contribution to a broader power portfolio. For example, while a solar resource may have a cheaper cost compared to wind on a $/kW of nameplate capacity basis or $/MWh basis, the wind resource may provide better value if evaluated on a $/kW of accredited capacity basis.

The impact of translating nameplate capacity value into accredited capacity value is not limited to renewable and storage resources. Accurately accounting for the reliability contributions of thermal resources is gaining more attention, especially as extreme weather events highlight what can go wrong for dispatchable, thermal resources. Thermal resources are subject to several limitations such as fuel supply constraints during extreme cold, derates during extreme heat, and other weather-related performance issues. Thermal generation remains a cornerstone to reliable power system operations; however, winter storms, extreme heat waves, and evolving accreditation methods have underscored that it is not “perfect capacity” either. It is therefore necessary to evaluate the resiliency offerings and strategies of generation technologies to ensure adequate performance. Taken together, these realities highlight the importance of planning for ever-changing accreditation frameworks when building a well-balanced resource portfolio that supports long-term reliability, affordability, and decarbonization goals.

Policy

Policy is also shaping the economics for clean energy resources. The One Big Beautiful Bill Act accelerates the wind and solar phase-out structure for 45Y Clean Electricity Production Tax Credits and 48E Clean Electricity Investment Tax Credits, with key deadlines tied to when projects begin construction and when they are placed in service. At the same time, longer runways remain intact for other technologies, such as energy storage. As such, the timing of federal incentives is becoming more consequential, especially for wind and solar projects. As those deadlines approach, project economics will become more sensitive to schedule delays, procurement timing, and supply chain execution. More broadly, resource planners must be prepared to make long-term decisions amid ongoing political uncertainty, making scenario planning an increasingly important tool for managing risk and preserving flexibility.

Conclusion

The challenging reality is that power supply decision-makers are facing a difficult future to plan for. Between rising electricity demand, tightened equipment markets, federal policy uncertainty, and evolving capacity accreditation rules, there are many sources of risk. To manage these risks, effective planning now requires a wider lens in which numerous factors, including, but not limited to, executable installed cost, development timeline, accreditation value, and exposure to future policy changes are jointly considered.

Waiting for more certainty can be an expensive option. The market signals coming from developers, OEMs, and reliability planners all point in the same direction: future generation decisions will be made in a world where dependable capacity is more valuable, supply chains are tighter, and project timing is a priority. “Wait and see” is becoming a less comfortable default. In many cases, the most prudent strategy is to begin planning earlier, test assumptions deliberately, and evaluate portfolios across a range of future scenarios. Above all, decision-makers must be ready to adapt because planning for the future grid requires a mindset that evolves as quickly as the market around it.